The poultry industry is a key source of protein and a vital part of the livestock economy. Over the past decade, with investments exceeding Rs 1,056 billion, it has achieved an average annual growth rate of 7.3%. The industry employs over 1.5 million people. Pakistan’s poultry industry ranks third in South Asia after India’s and Bangladesh’s, where production techniques have improved, and export markets have expanded. Globally, Pakistan is now the eighth-largest producer of poultry chicken, indicating strong potential for growth and development.

Thank you for reading this post, don't forget to subscribe!Industry Structure & Production Capacity

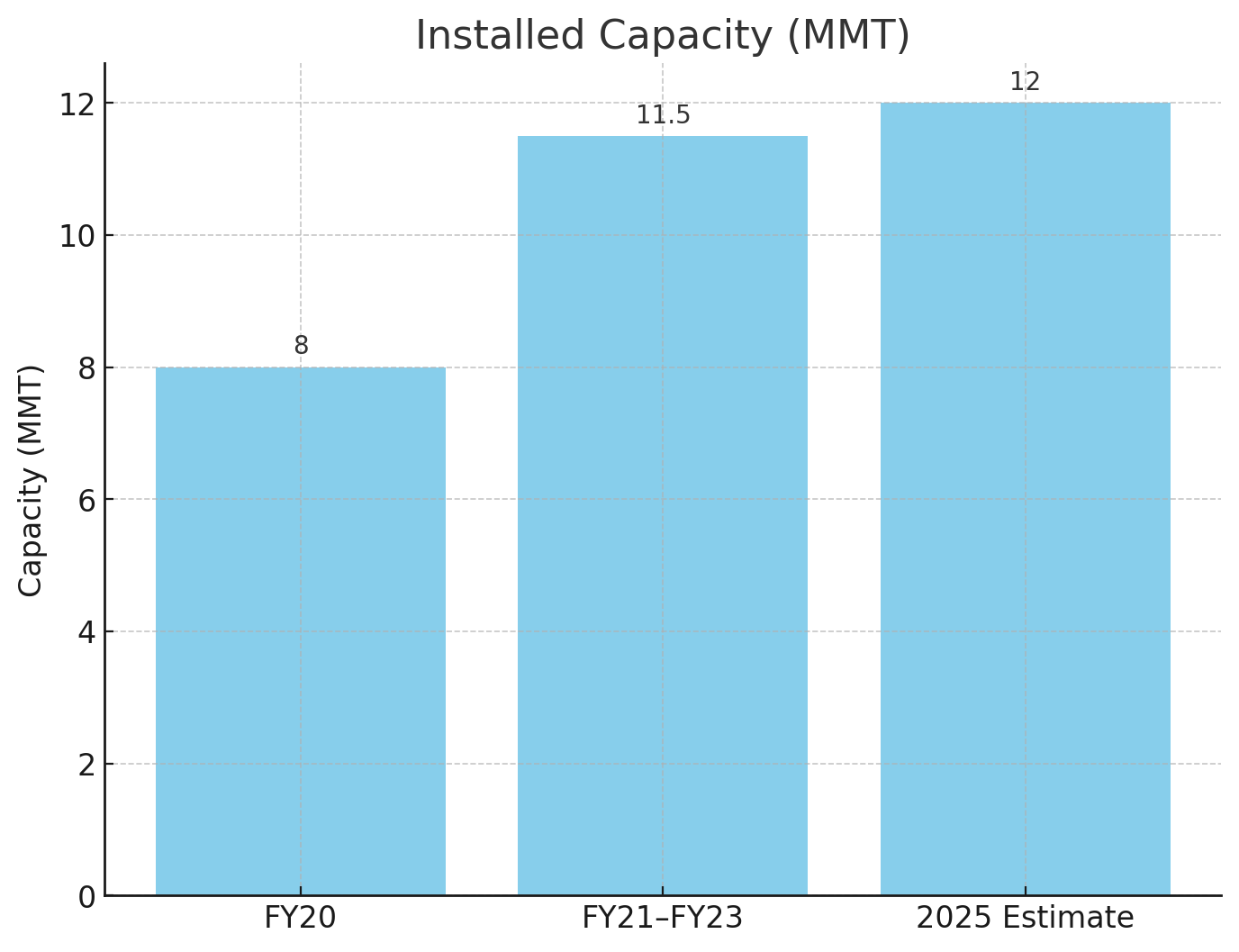

• As of FY23, Pakistan’s poultry feed sector comprised approximately 150 registered and 200 unregistered feed mills, collectively offering an installed annual capacity of 10–13 million MT, with utilization around 56% (PACRA).

• Earlier data from FY20 showed a slightly lower capacity of about 8 million MT, with utilization around 43% (PACRA).

• According to global trade estimates, there are nearly 300 feed mills with a combined output capacity of 12 million MT (aviNews, USDA Apps).

Feed Demand, Volume & Raw Material Dynamics

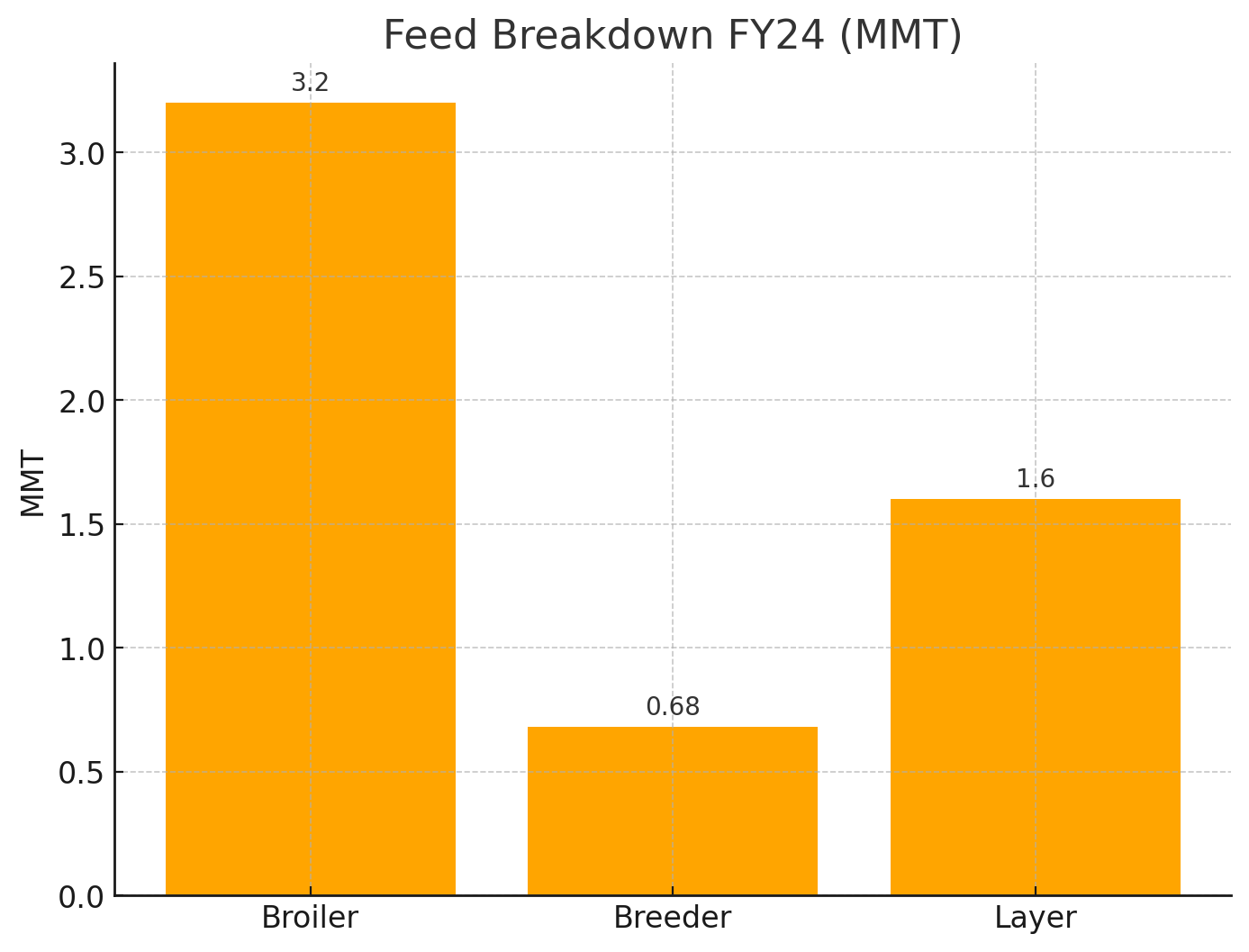

• Total feed consumption declined from 6.6 MMT in FY22 to 5.91 MMT in FY23, and further to 5.48 MMT in FY24 – a downward trend reflecting raw material price pressures and economic headwinds (PACRA).

Breakdown of FY24 consumption:

o Broiler feed: 3.2 MMT (↓ approximately 8.5%)

o Breeder Feed: 0.68 MMT

o Layer feed: 1.6 MMT (stable) (PACRA).

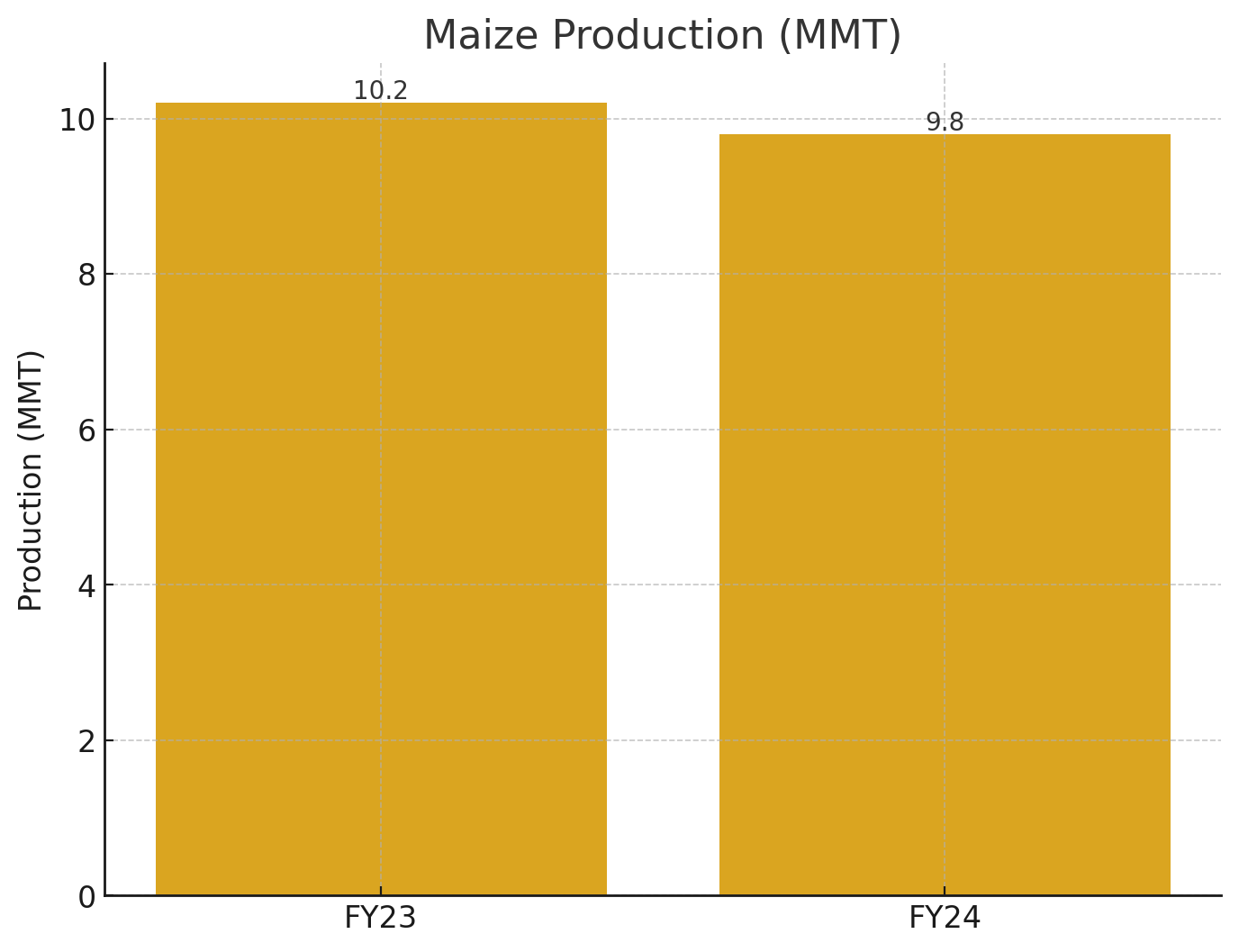

• Maize production decreased, falling from 10.2 MMT in FY23 to 9.8 MMT in FY24 – a 3.1% drop—while cultivation area shrank 4.5% (PACRA).

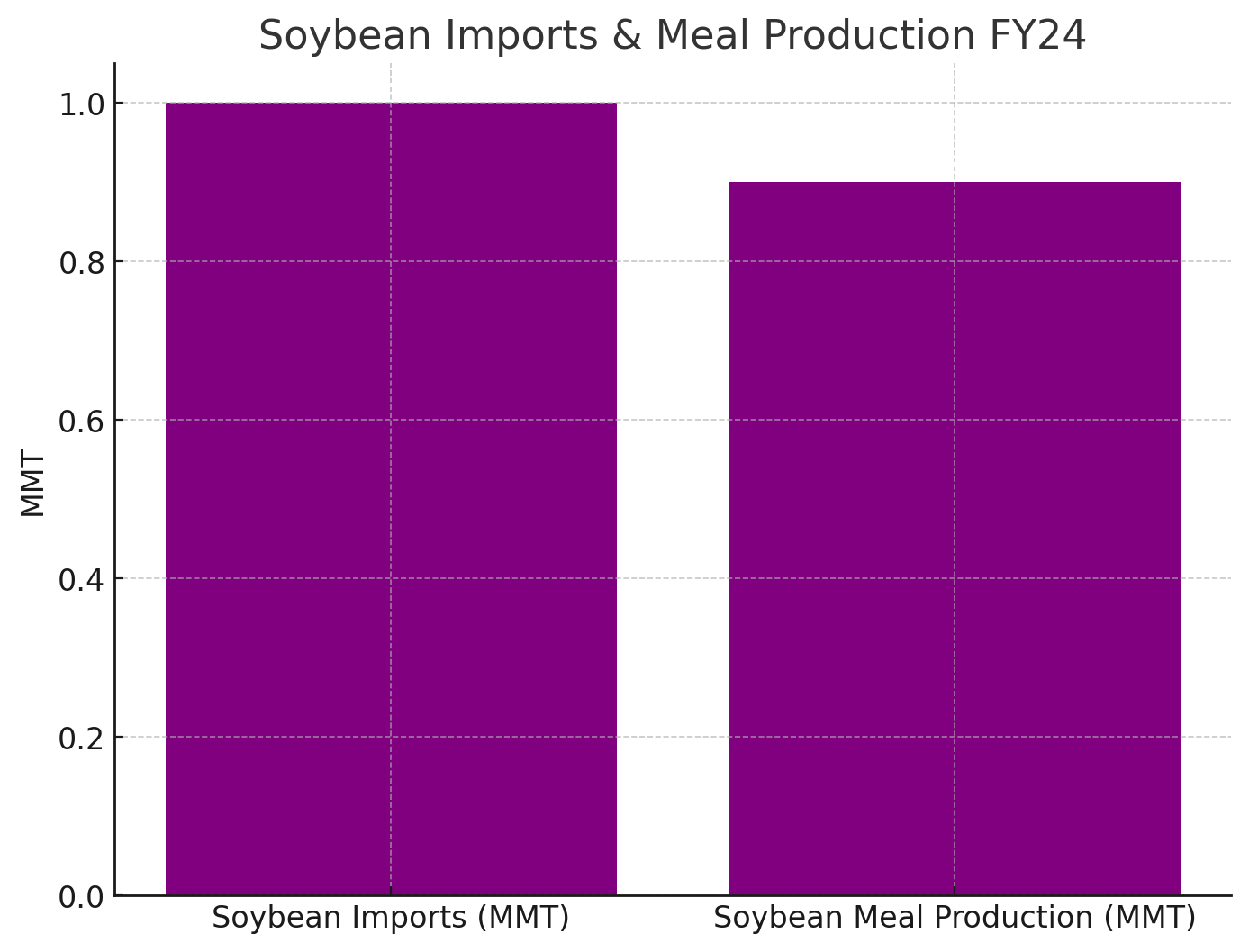

• Meanwhile, removal of GMO-related restrictions in late 2023 triggered a 38.6% jump in soybean seed imports (1.0 MMT) and increased soybean meal production by 145.9% to 0.9 MMT in FY24 (PACRA).

Financial Performance

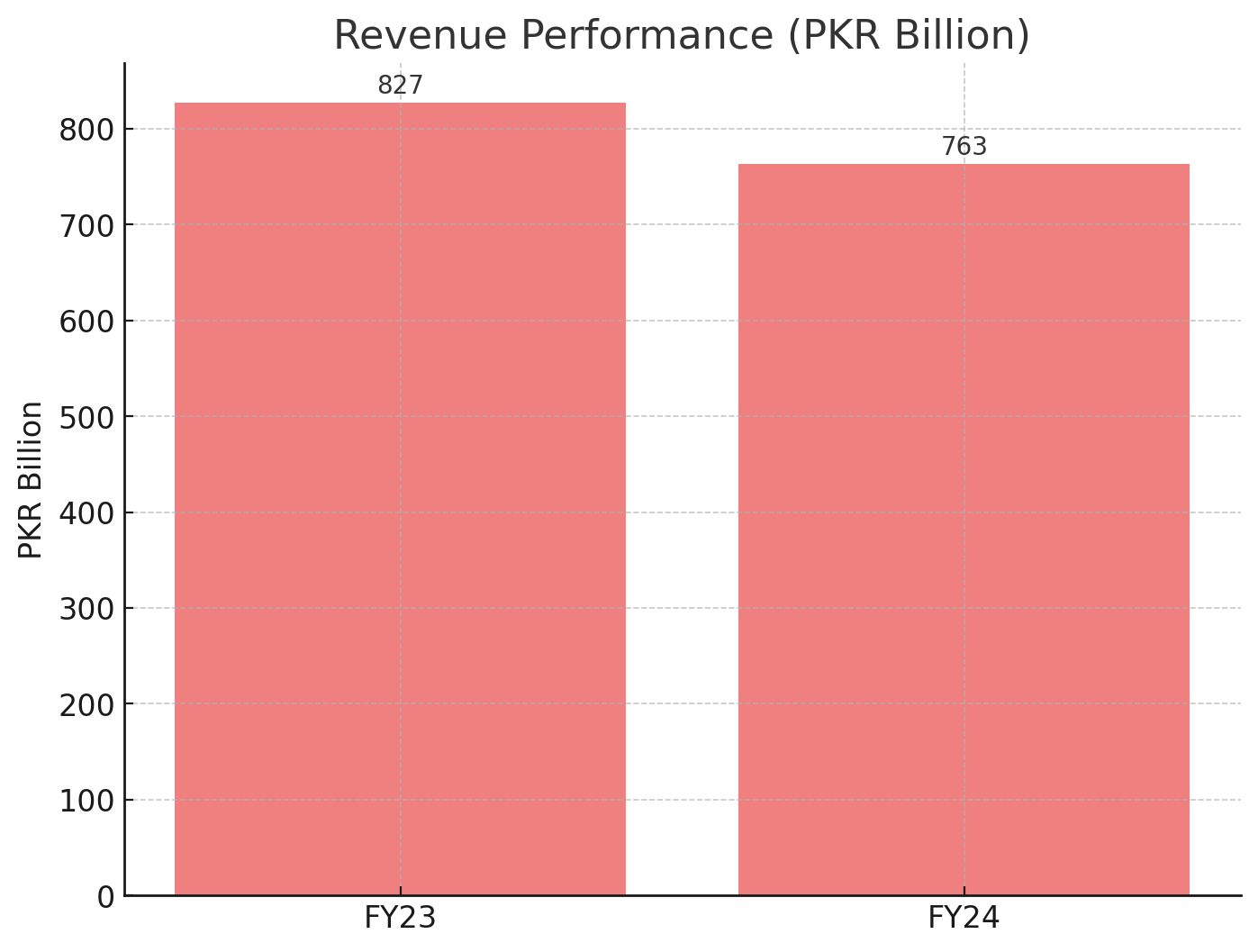

• Revenue grew sharply to PKR 827 billion in FY23 (+29%) but dipped to PKR 763 billion in FY24 (–7.7%) (PACRA).

• The sector’s GDP contribution hovered around 1.0% in FY23, moderating to 0.8% in FY24 (PACRA).

Total Capacity

|

Year |

Installed Capacity (MMT) |

Utilization (%) |

|

FY20 |

8 MMT |

43% |

|

FY21–FY23 |

10–13 MMT |

56% |

|

2025 Estimate |

12 MMT (300 mills) |

— |

• The growth in installed capacity—from around 8 million MT in FY20 to over 10 million MT in FY23—reflects significant industry investment (PACRA).

• The 12 million MT figure serves as a broader industry benchmark from trade data, likely incorporating both formal and informal mill capabilities (aviNews, USDA Apps).

Future Outlook & Prospects

Market Trends & Drivers

• Forecasts for the 2025/26 marketing year expect corn consumption (largely for poultry feed) to reach 9.1 MMT, supported by the rebound from soybean import policy changes (USDA Apps).

• The poultry feed market is projected to grow at a CAGR of 6.8% from 2025 to 2031, driven by demand for poultry meat and eggs, nutritional advancements, and rising incomes (6Wresearch).

• Pelletized feed is expected to dominate due to its efficiency and waste reduction benefits, especially among commercial producers (6Wresearch).

Industry Challenges & Risks

• Continued volatility in maize and soybean meal prices remains a critical challenge, with climate-sensitive maize production and global commodity swings impacting costs (6Wresearch, PACRA).

• Credit dependence adds financial fragility, particularly when demand drops or macroeconomic pressures intensify (PACRA).

Strategic Opportunities

• Diversification of feed ingredients using alternatives—like cottonseed, rapeseed, and sunflower meals—can reduce import dependence and stabilize input costs (PACRA, 6Wresearch).

• Adoption of pellet feed processing technologies, warehouse receipt financing, and stronger logistics can improve efficiency and margins (PACRA, 6Wresearch).

• Regulatory interventions—ranging from input import facilitation to quality control—could provide critical structural support.

• Sustained population growth, urbanization, and rising incomes buffer long-term demand, reinforcing poultry feed as a resilient segment.

Executive Summary

Pakistan’s poultry feed industry has grown from an underutilized 8 MMT capacity in FY20 to a robust 10–13 MMT infrastructure by FY23–24, with effective utilization still around 55–60%. Feed consumption dipped below capacity—5.48 MMT in FY24—due to raw material constraints and economic headwinds. However, the reinstatement of GMO soybean imports in late 2023 boosted raw material availability, notably increasing soybean meal production.

Looking ahead, corn consumption in feed is expected to reach 9.1 MMT in 2025/26, signaling a demand rebound. Market growth is forecast at 6.8% CAGR through 2025-2031, though achieving this will require addressing cost volatility, supply-chain frailties, and credit risks. Key growth levers include feed formulation innovations, ingredient diversification, modernization, and regulatory support.

Pakistan Poultry Feed Industry Overview

|

Category |

Details |

Source(s) |

|

Industry Size |

~150 registered & ~200 unregistered feed mills |

PACRA Jan’24 |

|

Total Capacity |

~10–13 MMT (FY23–24), ~12 MMT (2025 est.) |

PACRA Jan’24, Mar’25; USDA 2025 |

|

Utilization Rate |

~43% (FY20), ~56% (FY23) |

PACRA Jan’21, Jan’24 |

|

Feed Consumption (FY24) |

~5.48 MMT total: Broiler ~3.2 MMT (↓8.5%), Layer ~1.6 MMT (stable) |

PACRA Mar’25 |

|

Feed Consumption (FY23) |

~5.91 MMT (↓ from 6.6 MMT in FY22) |

PACRA Jan’24 |

|

Raw Materials – Maize |

Production: 10.2 MMT (FY23) → 9.8 MMT (FY24, ↓3.1%), cultivation area ↓4.5% |

PACRA Mar’25 |

|

Raw Materials – Soybean |

Import ban lifted in late 2023 → imports ↑38.6% (~1.0 MMT); Soymeal production ↑145.9% (~0.9 MMT) |

PACRA Mar’25 |

|

Revenue |

PKR 827 bn (FY23, ↑29%), PKR 763 bn (FY24, ↓7.7%) |

PACRA Jan’24, Mar’25 |

|

Future Corn Demand |

Forecast 9.1 MMT (2025/26, largely poultry feed use) |

USDA 2025 |

|

Market Growth Outlook |

Expected CAGR 6.8% (2025–2031) |

6WResearch |

|

Technology Trend |

Shift toward pelletized feed (efficiency, reduced waste) |

6WResearch |

|

Key Challenges |

Raw material price (maize, soybean), credit risk, weak regulations, rural logistics |

PACRA, 6WResearch |

|

Opportunities |

Ingredient diversification (cottonseed, rapeseed, sunflower), modern feed tech, regulatory support |

PACRA, 6WResearch |

Pakistan Poultry Sector – Broiler, Layer & Breeder Overview (in millions)

|

Category |

Broiler |

Layer |

Breeder |

Source(s) |

|

Population (FY24) |

1,350 |

185 |

11 |

PACRA Jan’24, Mar’25 |

|

Feed Consumption (FY24) |

3.20 |

1.60 |

0.68 |

PACRA Mar’25 |

|

Share in Total Feed |

58% |

28% |

11% |

PACRA Jan’24, Mar’25 |

|

Production Purpose |

Meat (5–6 weeks) |

Eggs (72 weeks) |

Parent stock for hatching eggs (supports broiler & layer industry) |

Industry reports |

|

Revenue Dependence |

High (volatile with market & prices) |

Moderate (stable egg demand) |

Indirect (critical for continuity of poultry supply chain) |

PACRA reports |

|

Key Risk Factors |

Feed price volatility, disease outbreaks |

Feed quality, disease, seasonal egg demand |

Biosecurity, genetics, disease management |

PACRA, industry |

|

Growth Prospects |

Driven by urban meat demand, rising incomes |

Stable growth with rising egg consumption |

Expansion tied to demand for day-old chicks (DOCs) |

PACRA, USDA |